LightGBM: Alpha for quantile regression doesn't seem to work

Hi there! I’ve been working with @ClimbsRocks on using auto_ml as a wrapper on top of lightgbm for a lot of our use cases at work. We’re super excited that lightgbm supports quantile regression. I saw earlier in #1036 that it looks like alpha issue was resolved, but when I pass in different alphas, I’m not seeing different results.

On my end, I wrote some functions to check if there were any difference between passing in alpha=.86 and alpha=.95 and I keep on getting results that were ~ 58th percentile as opposed to 86th or 95th on my validation and test sets.

@ClimbsRocks wrote something to test this:

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

## ADDED

import lightgbm as lgb

## END ADDED

from sklearn.ensemble import GradientBoostingRegressor

np.random.seed(1)

def f(x):

"""The function to predict."""

return x * np.sin(x)

#----------------------------------------------------------------------

# First the noiseless case

X = np.atleast_2d(np.random.uniform(0, 10.0, size=10000)).T

X = X.astype(np.float32)

# Observations

y = f(X).ravel()

dy = 1.5 + 1.0 * np.random.random(y.shape)

noise = np.random.normal(0, dy)

y += noise

y = y.astype(np.float32)

# Mesh the input space for evaluations of the real function, the prediction and

# its MSE

xx = np.atleast_2d(np.linspace(0, 10, 100000)).T

xx = xx.astype(np.float32)

alpha = 0.95

# clf = GradientBoostingRegressor(loss='quantile', alpha=alpha,

# n_estimators=250, max_depth=3,

# learning_rate=.1, min_samples_leaf=9,

# min_samples_split=9)

# clf.fit(X, y)

## ADDED

clf = lgb.LGBMRegressor(objective='quantile',

alpha=alpha,

num_leaves=31,

learning_rate=0.05,

n_estimators=100)

clf.fit(X, y,

eval_set=[(X, y)],

eval_metric='quantile',

early_stopping_rounds=5)

## END ADDED

# Make the prediction on the meshed x-axis

y_upper = clf.predict(xx)

# clf.set_params(alpha=1.0 - alpha)

# clf.fit(X, y)

## ADDED

clf.set_params(alpha=1.0 - alpha)

clf.fit(X, y,

eval_set=[(X, y)],

eval_metric='quantile',

early_stopping_rounds=5)

## END ADDED

# Make the prediction on the meshed x-axis

y_lower = clf.predict(xx)

# clf.set_params(loss='ls')

# clf.fit(X, y)

## ADDED

clf.set_params(objective='regression', eval_metric='l2')

clf.fit(X, y,

eval_set=[(X, y)],

eval_metric='l2',

early_stopping_rounds=5)

## END ADDED

# Make the prediction on the meshed x-axis

y_pred = clf.predict(xx)

# Plot the function, the prediction and the 90% confidence interval based on

# the MSE

fig = plt.figure()

plt.plot(xx, f(xx), 'g:', label=u'$f(x) = x\,\sin(x)$')

plt.plot(X, y, 'b.', markersize=10, label=u'Observations')

plt.plot(xx, y_pred, 'r-', label=u'Prediction')

plt.plot(xx, y_upper, 'k-')

plt.plot(xx, y_lower, 'k-')

plt.fill(np.concatenate([xx, xx[::-1]]),

np.concatenate([y_upper, y_lower[::-1]]),

alpha=.5, fc='b', ec='None', label='90% prediction interval')

plt.xlabel('$x$')

plt.ylabel('$f(x)$')

plt.ylim(-10, 20)

plt.legend(loc='upper left')

plt.show()

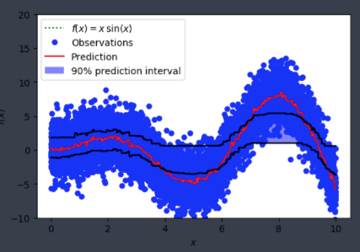

and was seeing something like:

Is alpha hardcoded in somewhere or is this user error on my end?

About this issue

- Original URL

- State: closed

- Created 7 years ago

- Comments: 15 (2 by maintainers)

@joseortiz3 because you might want to observe something else than quantile loss when performing quantile regression (such as mse, mae, etc. or a self-defined business metric). For a quantile task, in most cases you will watch the MSE metric and not the quantile metric.

@joseortiz3 The main difference is the leaf_output. Sklearn use the according percentile value as output, while LightGBM uses gradients (much smaller values) directly. As a result, you can use larger learning_rate, e.g. 0.3 or 0.4. You also can set

reg_sqrttoTrueto speed up the convergence.quantile_l2uses the second order gradients, so it will be faster. However, it is more easily over-fitting.